The UAE’s E-Invoicing Framework

Central to the UAE’s implementation of E-Invoicing is the adoption of the Peppol (Pan-European Public Procurement Online) framework, a globally recognised interoperability standard that enables the secure and standardised electronic exchange of business documents, including invoices, between different systems and parties.

The UAE has selected a 5-corner model, also known as the Decentralised Continuous Transaction Control and Exchange (DCTCE) model. Under this approach, the government does not operate a single central invoicing platform through which all invoices must pass. Instead, the system is decentralised, and Accredited Service Providers (ASPs) act as the technical interface between businesses and the Peppol network and must comply with UAE E-Invoicing requirements and complete mandatory testing in line with PINT-AE specifications.

The UAE’s chosen DCTCE model has two main parts:

-

Exchange of invoices:

When a business issues an invoice, the invoice data is generated from the business’s invoicing system and submitted to its Accredited Service Provider (ASP). The ASP validates the data to ensure it complies with the UAE E-Invoicing Data Dictionary and converts it into the UAE standard E-Invoice format. Once validated, the ASP transmits the E-Invoice securely over the Peppol network to the buyer’s Accredited Service Provider, which then delivers the invoice to the buyer’s systems.

-

Reporting to the tax authority:

In parallel with invoice exchange, the Accredited Service Provider reports the tax-related data fields from the invoice to the central government reporting system established under the UAE E-Invoicing framework by the Ministry of Finance and the Federal Tax Authority, through a separate reporting channel.

Businesses onboarded to the UAE E-Invoicing system will be listed in the Peppol Directory.

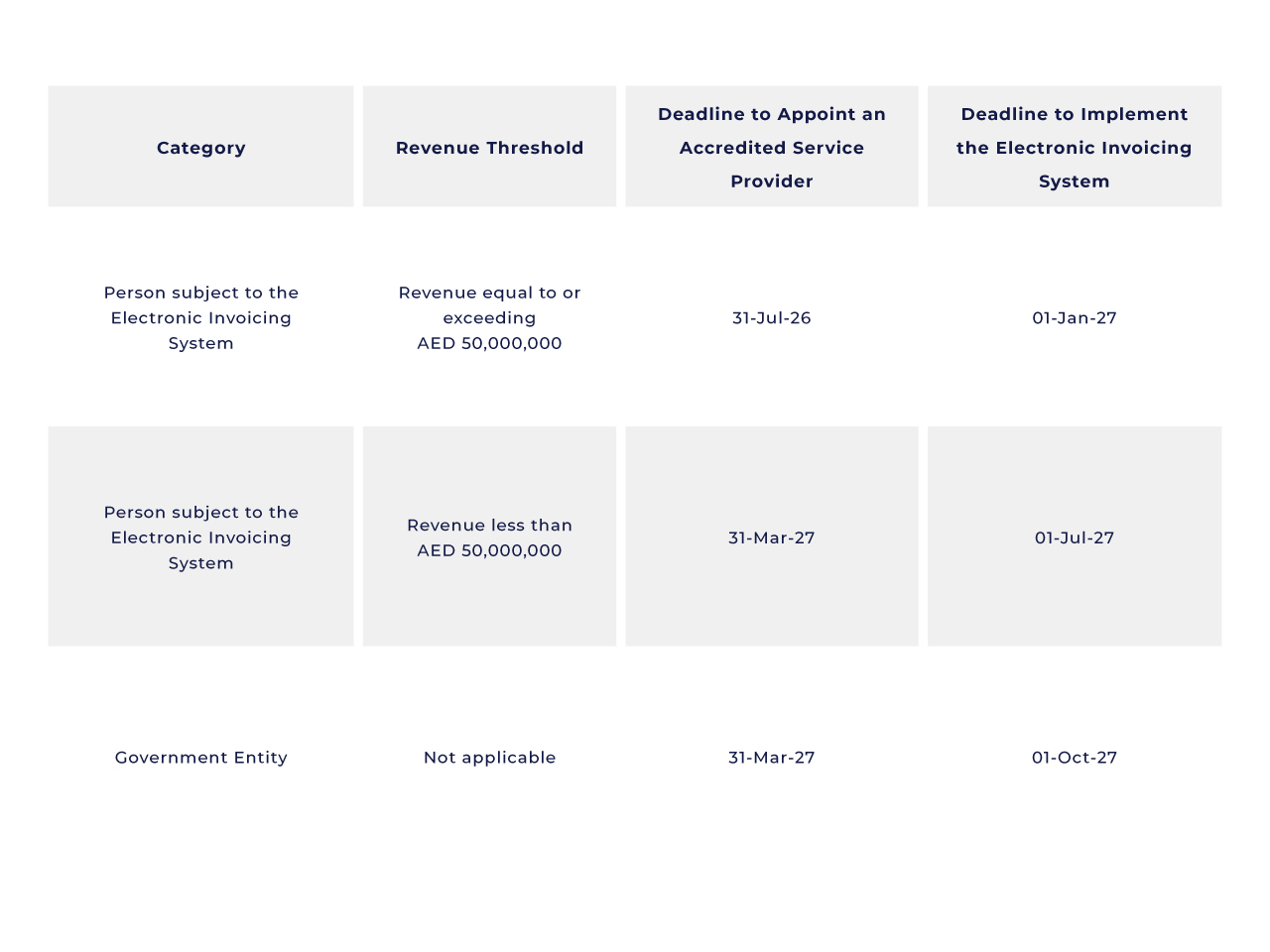

Implementation Phases and Timelines

Implementation of UAE E-Invoicing has been planned in phases, based on revenue thresholds and entity type. The important dates for businesses to remember are as follows:

It’s important to note that these are final deadlines by which businesses must appoint an Accredited Service Provider and complete implementation. The preparation phase, including system readiness, data alignment, testing, and internal coordination, can take a significant amount of time, so businesses should begin planning and implementation well in advance rather than waiting until the deadline.

Penalties for Non-Compliance

The UAE E-Invoicing regime sets out specific administrative penalties designed to discourage both delayed implementation and ongoing operational non-compliance. The penalties applicable under the framework include the following:

- Failure by the issuer to implement the Electronic Invoicing System on time, including failure to appoint an Accredited Service Provider within the prescribed timeline, attracts a penalty of AED 5,000 for each month of delay or part thereof.

- Failure by the issuer to issue and transmit an electronic invoice through the Electronic Invoicing System within the prescribed timeline attracts a penalty of AED 100 per invoice, capped at AED 5,000 per calendar month.

- Failure by the issuer to issue and transmit an electronic credit note through the Electronic Invoicing System within the prescribed timeline attracts a penalty of AED 100 per credit note, capped at AED 5,000 per calendar month.

- Failure by the issuer to notify the authority of a system failure within the prescribed timeline attracts a penalty of AED 1,000 for each day of delay or part thereof.

- Failure by the recipient to notify the authority of a system failure within the prescribed timeline also attracts a penalty of AED 1,000 for each day of delay or part thereof.

- Failure by the issuer or the recipient to notify the appointed Accredited Service Provider of changes to data registered with the authority within the prescribed timeline attracts a penalty of AED 1,000 for each day of delay or part thereof.

What Businesses Falling Under the UAE E-Invoicing Framework Should Do Now

Businesses that fall within the scope of the UAE E-Invoicing framework need to begin preparing for implementation by assessing their readiness and planning how E-Invoicing will be adopted across their operations. This includes carefully selecting and onboarding an Accredited Service Provider (ASP) and aligning systems, data, and internal processes with UAE E-Invoicing requirements. Some of the steps businesses need to take to comply with the regulatory requirements include:

- Understanding how UAE E-Invoicing works in practice, including how invoices are created, validated, exchanged, and reported under the Peppol-based 5-corner model, and how these fit with their existing ERP, billing, and finance systems, and if any significant changes are required.

- Reviewing the commercial and operational impact before finalising an Accredited Service Provider, looking beyond pricing to implementation timelines, internal effort, ongoing compliance responsibilities, and support requirements.

- Preparing internal systems and data for structured invoicing, with mandatory data fields available at source and processes capable of supporting validation and reporting. It is important to note that UAE E-Invoicing data standards require a significant number of mandatory fields, making early data assessment and collection critical.

- Planning and carrying out structured testing for invoice creation, validation, exchange, and reporting, including pilot testing, system integration testing, and user acceptance testing.

- Setting up clear ownership, controls, and monitoring to manage system issues, data changes, invoice failures, and notification requirements, particularly where penalties apply on a per-day basis.

AKW Consultants supports businesses across each of these steps. We assess data readiness, guide Accredited Service Provider selection, design and oversee system integrations, manage testing, and help businesses establish governance and controls to reduce the risk of penalties. Our role is to ensure E-Invoicing implementation is technically sound and aligned with the UAE’s regulatory expectations.