The New Regulatory Update

On 12th January 2026, the Dubai Financial Services Authority (DFSA) brought into force a materially updated Crypto Token framework for activities conducted in or from the Dubai International Financial Centre (DIFC). Under the new update, the DFSA has shifted from a DFSA-led suitability assessment to a firm-led suitability assessment for Crypto Tokens. Firms providing Financial Services involving Crypto Tokens must now determine, on a reasoned and documented basis, whether each Crypto Token they engage with meets the DFSA’s suitability criteria. As a direct consequence, the DFSA will no longer publish a list of Recognised Crypto Tokens.

In this article, we examine what Crypto Tokens mean under the DFSA regulatory framework, how different categories of Tokens are defined and distinguished, the regulatory requirements for assessing Crypto Token suitability, and the practical challenges and expertise required for firms to implement the new firm-led suitability regime in DIFC.

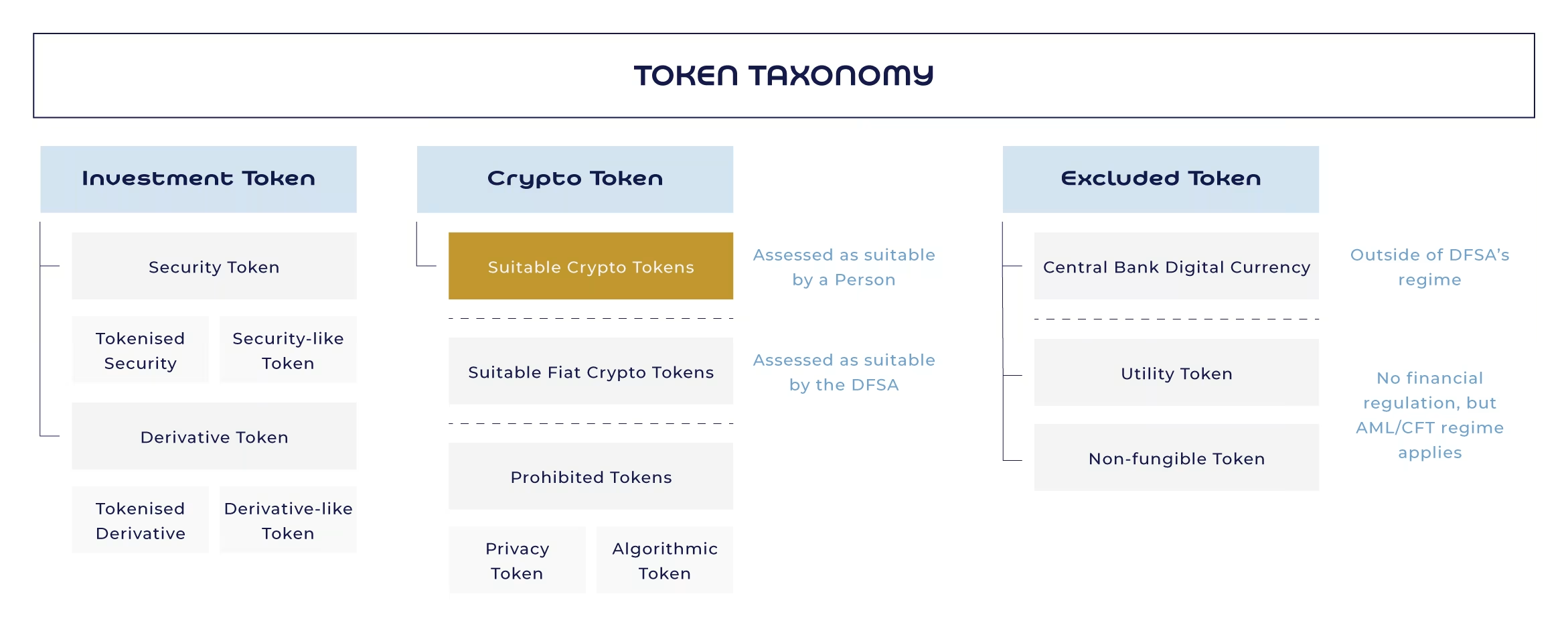

What is a Crypto Token under the DFSA framework?

Under the DFSA framework, a Token is classified as a Crypto Token if it:

- is used, or is intended to be used, as a medium of exchange or for payment or investment purposes; or

- confers a right or interest in another Token that meets the requirement above.

The Token’s “intended use” will normally be evident from developer materials such as the white paper or other concept papers prepared and published for the Token.

It is equally important to understand what does not qualify as a Crypto Token under the DFSA framework. A Token is not treated as a Crypto Token if it is classified as an Excluded Token, or as an Investment Token.

The DFSA expressly treats the following as Excluded Tokens:

- Non-Fungible Tokens (NFTs)

- Utility Tokens

- Digital currency issued by a government, government agency, central bank, or other monetary authority