Introduction

In today’s fast-paced financial domain, combatting illicit activities and fortifying defense against financial crimes have become indispensable. At the heart of these efforts lies the KYC (Know Your Customer/Client) process, a cornerstone in the fight against money laundering, terrorist financing, and other unlawful activities. KYC is a pivotal component of Anti-Money Laundering (AML) and Counter-Terrorist Financing (CFT) policies, holding the key to safeguarding the integrity of financial systems. This article delves into the significance of KYC within the United Arab Emirates (UAE), where both Financial Institutions (FIs) and Designated Non-Financial Businesses and Professions (DNFBPs) are mandated to adhere to stringent AML-CFT laws.

Compulsory Adherence in the UAE’s Financial Landscape

The UAE underscores the imperative nature of KYC by mandating its implementation for both FIs and DNFBPs as part of its AML-CFT regulations. DNFBPs, spanning auditors, real estate agents, dealers of precious metals and stones, and trust and corporate service providers, wield considerable influence within the economy despite their indirect engagement in traditional financial activities. By adopting the KYC process, these entities gain the ability to discern the authenticity of their clientele, thus insulating themselves from the pervasive network of financial crimes.

The Essence of KYC

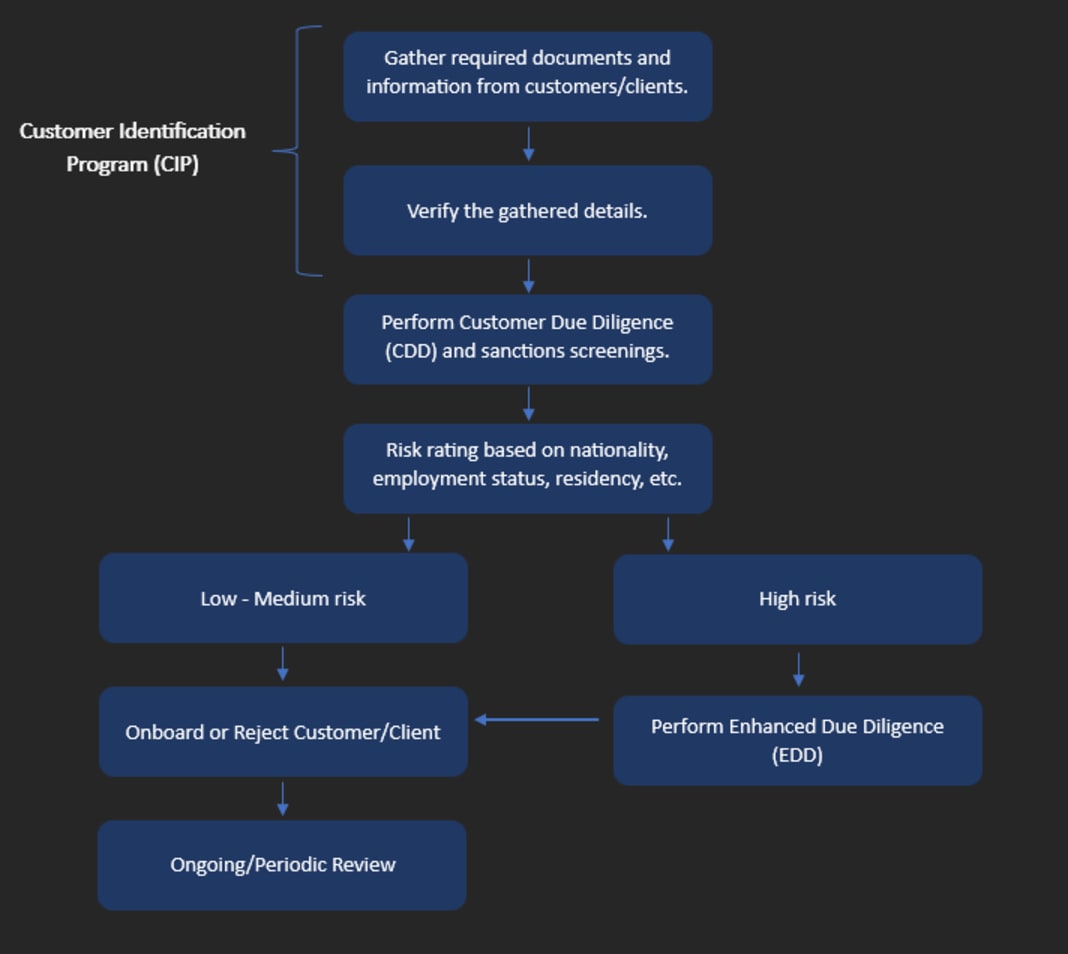

Beyond a procedural formality, KYC is an intricate procedure involving the meticulous verification of customer identities alongside the assessment of potential risks. This critical scrutiny takes place during the onboarding process and persists throughout the customer relationship. By establishing a customer’s identity and constructing a comprehensive risk profile, especially for entities susceptible to financial misconduct, KYC provides invaluable insights. This empowers businesses to engage exclusively with bona fide individuals and legitimate organizations, mitigating risks and preserving their reputation.

Conducting the KYC and Customer Due Diligence (CDD) procedure is imperative under various circumstances:

- Commencing a new business relationship.

- Executing sporadic transactions exceeding designated thresholds.

- Possessing suspicions of money laundering or terrorist financing.

- Questioning the adequacy or accuracy of previously obtained customer identification data.

- Necessitating additional information from existing customers based on account conduct.

- Experiencing changes in signatories, beneficial owners, or other key personnel.

Should customers fail to meet these requisites, DNFBPs are encouraged to:

- Refrain from initiating business relations, conducting transactions, or opening accounts.

- Terminate the existing business relationship.

- Contemplate filing a report concerning suspicious transactions related to the concerned customer.

As the first step in AML and CFT policy, KYC is a crucial stage in preventing illegal activities

Unveiling Suspicious Accounts

In the UAE’s unwavering commitment to eradicating money laundering, DNFBPs play a pivotal role in uncovering suspicious accounts that may be conduits for illicit funds. Adhering rigorously to the KYC process enhances their capacity to detect tell-tale signs and enact precautionary measures. In a financial landscape rife with evolving tactics, the vigilance enabled by KYC emerges as a potent weapon against the craftiness of criminal minds.

Distinguishing AML and KYC

While often used interchangeably, the realms of AML and KYC bear important distinctions. AML encompasses a comprehensive framework aimed at ensuring compliance, preventing fraud, and identifying transactions that arouse suspicion. On the other hand, KYC focuses on the meticulous verification of customers and risk assessment. Both elements synergize to form an essential nexus in the realm of financial security, countering criminal endeavors and preserving the sanctity of the financial ecosystem.

Conclusion

As the UAE’s financial landscape undergoes rapid expansion, the spectre of financial crimes looms larger. KYC emerges as a critical tool in the fight against money laundering and terrorist financing. Through thorough identity verification, risk profiling, and consistent vigilance across customer interactions, DNFBPs and FIs play a pivotal role in fostering a more secure financial environment. In this dynamic milieu, the interdependence of KYC and AML-CFT frameworks stands as an imperative bulwark against criminals seeking to exploit vulnerabilities and launder ill-gotten gains. By steadfastly adhering to KYC practices, the UAE’s financial sector reiterates its commitment to ethical conduct and fortified defense against financial transgressions.